Within the framework of the EU´s sustainability objectives and the its commitment to becoming helping the region to become climate-neutral by 2050, under the European Green Deal, new Directives have emerged. Among these directives are the Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD).

Both directives follow the EU´s sustainability standards.

In this blog, we delve into the interconnection between these directives, their distinctions, and the significance they hold.

But first, in the context of the European Union, what is a directive?

As a directive, to achieve the goal set, each member state may decide how to achieve it. The national law is needed to do so and gives the member state a lot more room to choose their own approach.

Second, we have been saying that this movement is a trend “bit-by-bit” and these directives are being implemented gradually across various types of companies, rolled-out in phases. If you own a small business and you want to better understand the impact of ESG aspects on your market, please get in touch.

You can also access our Industry Insights and our blog about ESG on Small Business. Early compliance can be a game changer in your business!

Ok, Let’s get this:

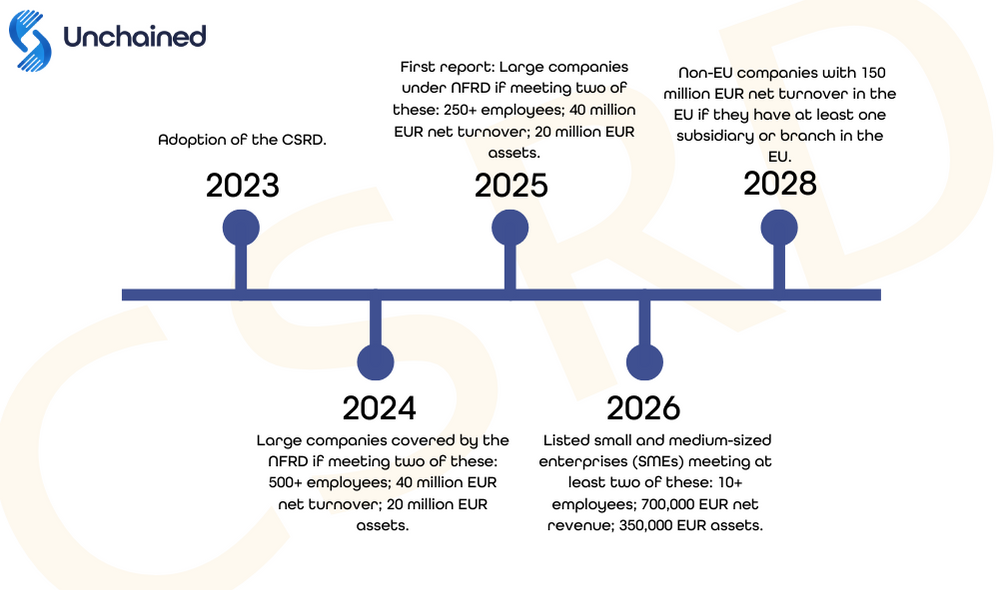

About Corporate Sustainability Reporting Directive (CSRD)

- Is an upgraded replacement of the EU Non-Financial Reporting Directive (NFRD).

- Is a new framework for sustainability reporting.

- Is EU centric.

- Came into effect in January 2023, but companies need to start reporting in 2024.

- Is mandatory for around 50.000 companies operating in the European Union.

- All the companies under CSRD are required to follow the directive´s reporting standards (ESRS – European Sustainability Reporting Standards*)

- Focuses on a transparency and disclosure reporting.

- Reporting scope: to report not only in a company’s own operations, the CSRD requires organisations to report on their entire value chain.

- Mandatory due diligence: Be prepared to disclose on your due diligence processes and results.

- Second opinion: companies need to get “limited” assurance for their sustainability program from a trustworthy third party.(They will review the data to make sure it’s accurate and legitimate.)

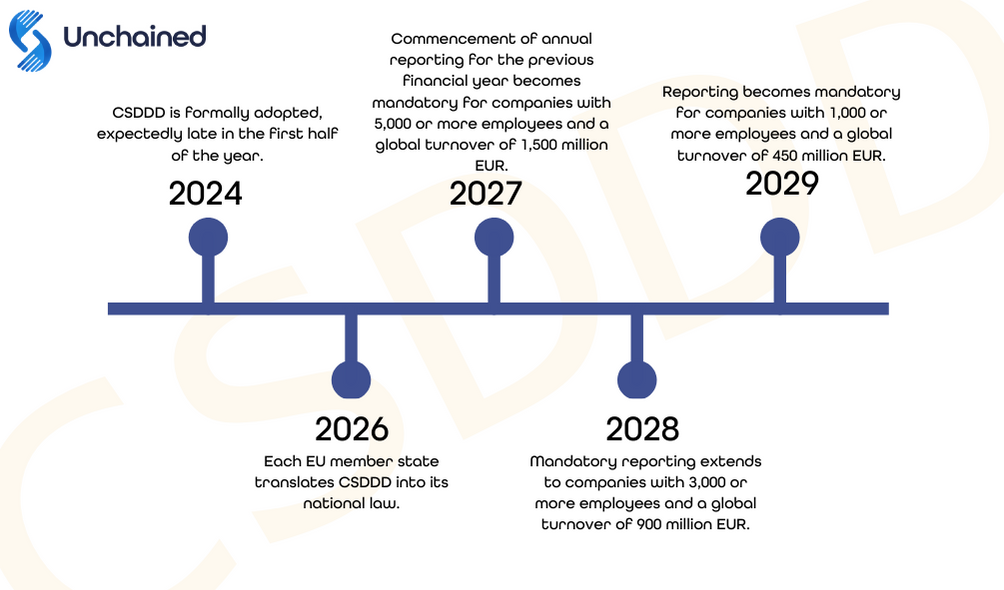

About Corporate Sustainability Due Diligence Directive (CSDDD)

- Is the first EU directive that requires companies to be much more transparent and accountable for everything they do.

- Focuses on the integration of due diligence into policies, risk management systems and at all relevant levels of a company’s operations.

- Companies need to create a plan and timeline for identifying and addressing human rights and environmental impacts.

- Applies to entities operating inside and outside the EU.

- Companies need to implement a plan to ensure that the business strategy is compatible with limiting global warming to 1.5°C in the line with the Paris Agreement.

- It targets larger companies, especially those in high-risk sectors, with the intention of enforcing proactive management, where the companies adopt and implement sustainable business practices.

In case of non-compliance, each member country has the autonomy to determine appropriate sanctions. However, the EU has proposed recommended administrative sanctions as public disclosure and monetary penalties.

The main difference lies in their focus and purpose:

- Corporate Sustainability Due Diligence Directive (CSDDD) primarily focuses on assessing and managing sustainability risks within the supply chain, emphasizing the responsibility of companies to prevent and mitigate adverse impacts on people and the environment.

- Corporate Sustainability Reporting Directive (CSRD) primarily concentrates on improving the quality, comparability, and reliability of sustainability reporting by companies, aiming to enhance transparency and accountability regarding environmental, social, and governance (ESG) matters in corporate disclosures.

In short, the CSRD is a reporting framework with guidelines on how companies should communicate. These guidelines are set out in the European Sustainability Reporting Standards* (ESRS). It is within the EU and gives to stakeholders a complete and easily understandable view of a company’s sustainability performance. The CSDDD is a required due diligence that steps that companies must take, legally obligated the environment and human rights. It includes both: EU and non-EU companies.

So, with the CSDDD, companies drive environmental and social responsibility, while the CSRD ensures European companies are transparent about it. These directives go hand in hand, and if a company falls under both, the idea is that they can implement them together for maximum impact.

Both are based on the OECD Guidelines for Multinational Enterprises and the UN guiding principles on Business and Human Rights.

*The European Sustainability Reporting Standards (ESRS) is the set of standards that companies subjected to the CSRD are required to follow.